“Instant Approval! Get Life Insurance in Minutes. No Needles, No Nurses.”

The ad glowed on the tablet in Sarah Miller’s hands. For Sarah, the 39-year-old part-time graphic designer and full-time manager of the family budget, the words were like a siren song. She and her husband, Mike, were deep in the process of getting life insurance, and it felt like anything but “instant.”

Mike, a 40-year-old software engineer, had just scheduled his paramedical exam. He wasn’t thrilled about the fasting, the questions, or the blood draw.

“Mike, look at this,” Sarah said, sliding the tablet across the kitchen table. “Why are we jumping through all these hoops? It says we could get approved today. Are we doing this wrong?”

It’s a tempting proposition. In a world of one-click ordering and instant gratification, the traditional life insurance process can feel slow and invasive. But is skipping the line worth the price? Does convenience come with a hidden cost?

Today, we’re going to pull up a chair with the Miller family as they explore the world of no medical exam life insurance and find out if it’s a smart shortcut or a costly mistake.

Your Guides for Today: The Miller Family

To make things simple, we’re using a fictional family to explore this topic.

- John & Mary (60s): The retired grandparents, focused on preserving their wealth and legacy.

- Mike & Sarah (40s): The parents, navigating their peak earning years, a mortgage, and saving for the future.

- Leo & Emily (Teens/Kids): The next generation, learning the basics of money.

This box is skippable for regulars but invaluable for newcomers.

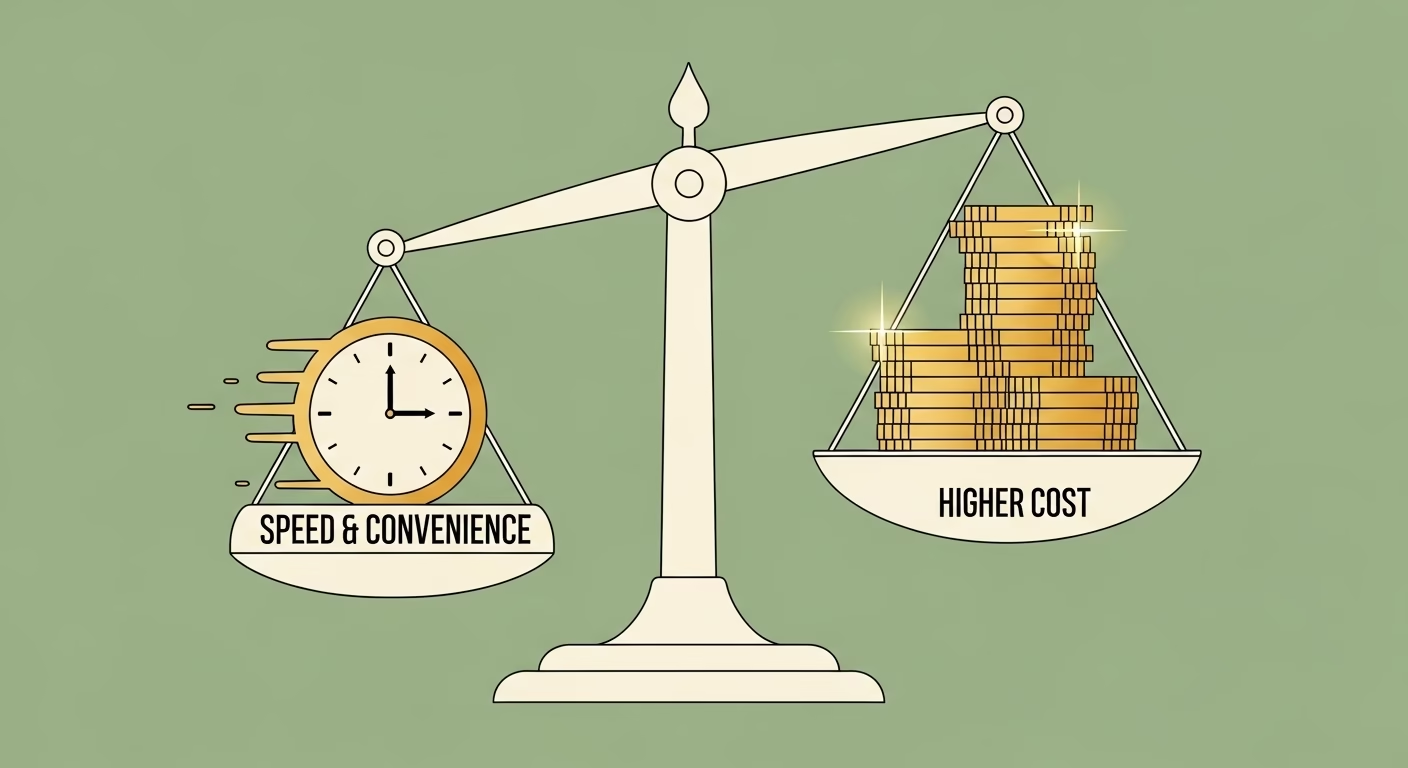

The Big Question: Why is No-Exam Insurance More Expensive?

The appeal of that online ad was undeniable. But her father-in-law, John, the cautious 68-year-old retiree, overheard them and offered a piece of wisdom from his factory days.

“When you buy parts for a machine without inspecting them first, you have to assume some might be faulty. So you pay a premium for the risk,” John said. “It’s the same with insurance. When they can’t inspect your health, they have to assume there’s more risk. And they charge you for it.”

He hit on the core principle. Life insurance is a business of risk assessment. A fully medically underwritten policy gives the insurer a clear, detailed snapshot of your health. With that data, they can confidently calculate your risk and give you the best possible price.

When you remove the medical exam, the insurer is flying blind. To protect themselves from this uncertainty (what they call adverse selection), they do two things:

- Charge a significantly higher premium.

- Limit the amount of coverage you can buy.

You’re paying a steep price for the convenience of skipping the exam.

The Two Main Types of No-Exam Policies

As Mike and Sarah started digging, they realized there are two very different kinds of life insurance without a medical exam, each with its own rules and trade-offs.

1. Simplified Issue Life Insurance

This is the most common type you see advertised for younger and middle-aged adults. It’s faster, but it’s not a complete free-for-all.

- How it Works: You skip the physical exam (no blood or urine samples), but you still have to answer a detailed health questionnaire. You also grant the insurer permission to instantly pull data from third-party sources, like your prescription drug history from the MIB Group (formerly Medical Information Bureau) and your driving record.

- Who It’s For: Generally healthy people who want to avoid the hassle of an exam and need coverage quickly.

- The Big Catch: You can absolutely be denied. If your health history reveals serious pre-existing conditions like a recent heart attack, cancer treatment, or uncontrolled diabetes, your application will likely be rejected.

2. Guaranteed Issue Life Insurance

This is the truest form of “no questions asked” coverage, but it’s a niche product designed as a last resort.

- How it Works: As long as you fall within the eligible age range (typically 50-85), you cannot be turned down for health reasons. There are no health questions and no medical background checks.

- Who It’s For: People with serious, chronic health problems who cannot qualify for any other type of insurance, or seniors looking for a small policy to cover final expenses.

- The Big Catches (and they are significant):

- Extremely High Cost: This is by far the most expensive type of life insurance per dollar of coverage.

- Low Coverage Amounts: The death benefit is usually very small, often capped between $5,000 and $25,000. It’s designed to cover final costs, which the National Funeral Directors Association (NFDA) reports can easily exceed $9,000.

- The Graded Death Benefit: This is the most critical feature. Most policies have a 2-3 year waiting period. If you pass away from natural causes during this time, your beneficiary does not get the full death benefit. They only receive a refund of the premiums you paid, plus 5-10% interest.

The Real Cost of Convenience: A Side-by-Side Comparison

To get a clear answer, Sarah, the family’s budget manager, decided to run the numbers. She got a quote for a $1 million, 30-year simplified issue policy for Mike. Then, she compared it to the quote he’d already received for a fully medically underwritten policy, for which he was healthy enough to qualify.

The results were staggering.

| Feature | Mike’s Traditional Policy (with Exam) | Simplified Issue Policy (No Exam) |

| Monthly Premium | $78 / month | $195 / month |

| Total 30-Year Cost | $28,080 | $70,200 |

| Coverage Limits | High (Up to $10M+) | Lower (Often capped at $1M or less) |

| Approval Time | 3-5 weeks | 24-48 hours |

| The Wiselix Verdict | Best for healthy applicants. The patience pays off with massive long-term savings. | A costly convenience. Only consider if you have a specific, urgent need and are willing to pay the premium. |

The convenience of a no-exam policy would cost their family an extra $42,120 over the life of the policy. For them, seeing the numbers in black and white made the decision obvious.

“That’s an entire car,” Mike said, astonished. “Or a huge chunk of college savings for Emily. I can handle a 30-minute exam for that.”

This exercise helped them understand that deciding between Term vs. Whole Life was only the first step; choosing the right application process was just as important financially.

Your 3-Step Reality Check

Before you opt for convenience, run this simple check to see if no medical exam life insurance is worth it for you.

- Assess Your Health Honestly. Are you a non-smoker in generally good health? If so, the medical exam is your golden ticket. It’s the key that unlocks the most affordable rates from the best insurers. Don’t pay the premium of a high-risk person if you aren’t one.

- Calculate Your True Need. No-exam policies often have lower coverage caps. Use a method like DIME to figure out how much life insurance you actually need. If you need $1.5 million but the no-exam policy caps out at $500,000, it’s not the right tool for the job.

- Compare Real Quotes. Don’t guess. Use a free online quoting tool to compare the price of a traditional term policy against a no-exam policy for the exact same coverage amount. Seeing the numbers side-by-side makes the decision clear.

Conclusion: A Specific Tool for a Specific Job

In the end, Sarah closed the ad on her tablet. The allure of “instant” had faded in the face of hard numbers. For the Millers, a healthy family looking for the most protection for the lowest cost, a medically underwritten policy was the clear winner. The small investment of time and patience would save their family a fortune.

No medical exam life insurance isn’t a scam; it’s a specific tool for a specific audience. It’s a crucial safety net for those with significant health conditions or for someone needing a small amount of coverage with extreme speed. But for the vast majority of families, the convenience is simply not worth the cost.

Frequently Asked Questions about No-Exam Life Insurance

1. What is the main difference between simplified issue and guaranteed issue?

Simplified issue requires you to answer health questions and can deny you based on your electronic health records. It’s for generally healthy people. Guaranteed issue asks no health questions and cannot deny you, but it’s much more expensive and has a 2-3 year waiting period for the full benefit. It’s for those with serious health issues.

2. Can you be denied no medical exam life insurance?

Yes. You can easily be denied for a simplified issue policy if you have significant pre-existing health conditions like recent cancer, heart disease, or a poor driving record. You cannot be denied for a guaranteed issue policy due to your health.

3. Is no medical exam life insurance a good idea for seniors?

It can be. For a senior in poor health who needs a small policy to cover final expenses, a guaranteed issue policy is often the only option and provides great peace of mind. For a healthy senior, a traditional short-term or permanent policy will still be more affordable if they can qualify.